Gold’s siren song has rung through the ages; countless men have lost their lives and sanity in search of it. Today, they lose their money instead. For the past decade, gold bugs have been dragged through the mud, as “bullish fundamentals” continue to accumulate. And it’s not just the doomers and newsletter writers that inexplicably inundate the space, or the hapless retail investors, that have been caught offside, but even the most credible institutions. I’m no stranger to gold fever myself; my 2022-2023 $SLV options are practically zeroed out.

Even in the midst of this wreckage, I’m not particularly excited about the space right now (and probably never will be), but I am tepidly positive going forward. I’ll detail my thoughts on where gold is headed.

Gold: The stories

Gold doesn't produce any cashflows; its value is pure narrative. I won’t belabor the narratives, as every single newsletter writer has repeated them ad nauseum, but I’ll briefly detail the main ones.

Inflation hedge

As the story goes, the salary of a roman centurion purchases just as much gold as that of a US captain today; gold seems to have the ability to retain, across millennia, purchasing power.

This sensitivity to inflation is backed up by recent data; backtesting with regressions of monthly returns on inflation shows that gold has an inflation beta of 2 from 1970-2020 (i.e. given a 1 point increase in CPI, gold price will rise by 2 points), matched only by Treasury Inflation Protected Securities (TIPS) and exceeded only by commodities (which have a beta of 4).

While inflation is notoriously difficult to predict, I believe there are very compelling reasons for it to be at least higher than the past 2 decades of disinflation:

End of long term debt cycle

Commodity scarcity

Deglobalization of supply chain

Reduction in labor supply

Long term debt cycle: Governments, over the long term, suppress interest rates and increase fiscal spending until debt levels reach unsustainable levels and interest rates reach the zero bound. When this happens, governments can choose either a deflationary style collapse where income is diverted towards debt repayments, or they can inflate the debt away through increased stimulation and interest rate suppression. The incentives are strongly skewed to the latter (51 out of 52 countries that reached sovereign debt levels of 130% of GDP ended up “defaulting”, either through devaluation, inflation, restructuring, or outright nominal default). We already see irresponsible spending in the US and ROW, as rising inequality, populism and political degeneracy results in complete antipathy to short term economic pain. A deflationary spiral is also a national security vulnerability in a multipolar world.

Commodity scarcity: Commodity capex is low, resource nationalism and weaponization is on the rise and commodity prices are and will continue rising.

Deglobalization of supply chain: Between 1980-2020, Chinese exports grew from US$11B to US$2.72T (14.7% CAGR). India’s grew at 9.9% CAGR for the same time period. This was a one time demographic and industrialization dividend that allowed for a period of sustained expansion of the monetary base without inflation. As this growth slows, and geopolitical tensions lead to increasing reshoring and duplication of supply chains, I expect inflation to be higher than in the past.

Reduction in labor supply: As populations age, and immigration slows due to increasingly populist policies (it’s estimated Trump’s nativism has cost the US 2M service jobs), labor supply will fall, increasing cost of both goods and services.

Overall, gold somewhat hedges inflation, and inflation looks to at least be higher in the future.

Debasement hedge

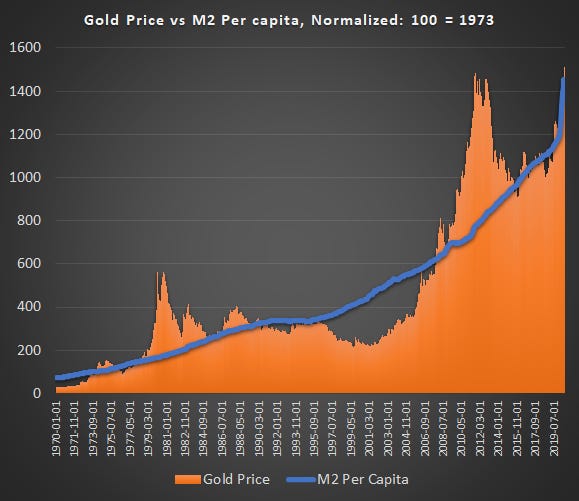

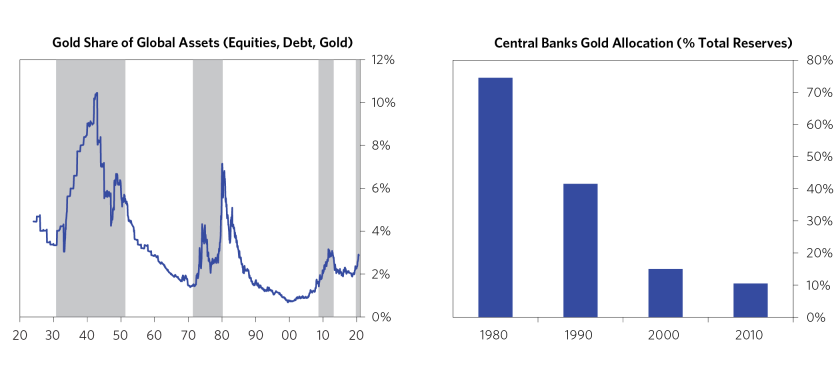

Long term debt cycles typically end via expansions of money supply. We have seen strong money supply growth throughout this cycle and I expect this trend to broadly continue. Gold price has tended to track money supply growth over time, albeit imperfectly.

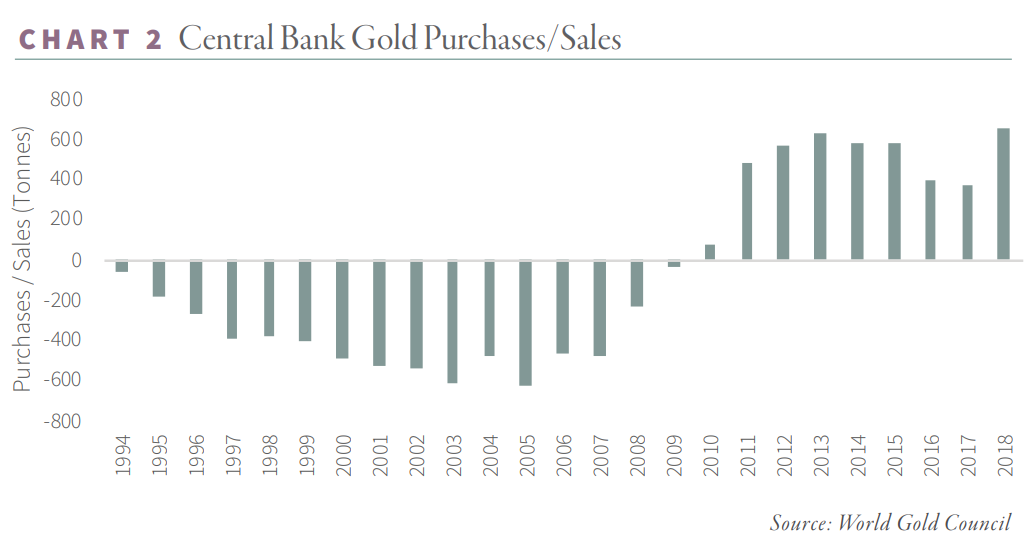

The debasement is significant not merely to retail investors who see their fiat lose purchasing power, but to sovereigns as well. The USD is world’s reserve currency, and net exporters around the world like China, Russia, Germany and Japan recycle their trade surpluses into treasuries which they store on the balance sheet for future uses (e.g. oil purchases). The implicit agreement is that the USD has to preserve the purchasing power of its currency so that their trading partners are not trading their goods for worthless pieces of paper. That compact is starting to break, firstly because of devaluation, and secondly because of the weaponization of USD. On the first point, the US has increasingly chosen the path of debasement and domestic stimulus over its obligations to its trade partners. In 2009, in response QE, the governor of the PBOC called in no uncertain terms for a new international reserve currency that is “disconnected from individual nations and able to remain stable in the long run, thus removing the inherent deficiencies caused by using credit-based national currencies”. On the second point, the US froze US$300B of Russian reserves. For major creditor countries like China that require reserves to exchange for what they need, this is a major threat. Overall, I see a move by central banks towards alternative currencies, particularly gold, which remains no one else’s liability:

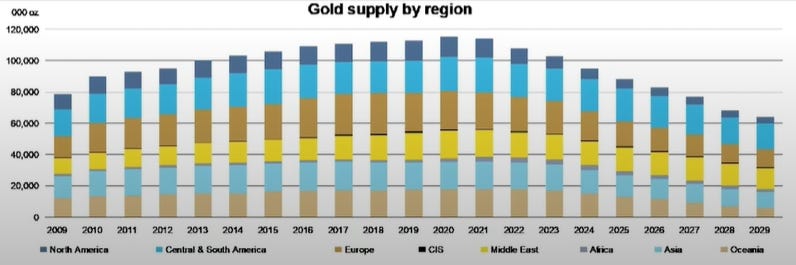

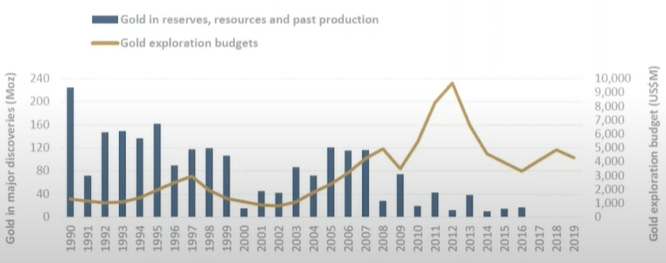

Physical supply falling

Essentially, current mines are depleted, grades are falling (hence higher costs) and there is not enough exploration to replenish those mines. There is increasing resource nationalism, meaning there are fewer places where gold can be mined safely.

Artificial suppression

Due to the large futures market, short term fundamentals can be overruled by big money. But physical inventories appear to be draining and there’s a thought that at some point, a physical shortage will begin to matter. And the papers position can also reverse.

The issues with the stories

The difficulty of predicting macro

The macro indicators that gold tracks are notoriously difficult to predict. The first derivative is hard enough; almost everyone has been wrong on inflation the past 2 yeas. The second derivative, which is potentially even more important, is even harder to track.

Tracking issues or “It doesn’t matter until it matters”

It is not merely the rate of change or the rate of change of the rate of change that is difficult to predict, the rate of change of gold to those rates are tenuous at best. Most of gold’s arguments have been around for years, to the total indifference of investors.

Inflation: in Verdad’s 1970-2020 backtest, only 25% of gold’s return variability is explainable by inflation (a significant, but modest, correlation of 0.5). Examining the 1970-1980 period of inflation and the 1980-2020 period of disinflation individually, the correlation falls from 0.61 to 0.26, meaning only 6.76% of gold’s variance in the past 40 years has been explained by inflation.

Monetary debasement: From the chart above, there was a period from late 90s to 2008 where gold did not track money supply growth at all.

Thus, on a monthly to even 5 year horizon, its very difficult to predict the reaction of gold prices to its “fundamentals“.

The supply side illusion

Structurally, gold has never had the best setup for supply and demand.

Firstly, the annual non investment demand for gold is something like 2/3 of annual mine production, meaning that investors have to purchase 1/3 of annual mine production annually merely to sustain the price. Furthermore, the non investment demands for gold are probably stagnating or decreasing.

Secondly, gold has an enormous stock to flow ratio. Almost all the gold we ever mined for investment or non investment demand is still with us, unlike say oil that is burned off every year. At higher prices, these will get recycled, and stock becomes supply. This creates enormous overhang for gold to push to higher price levels.

Opportunity cost

Because gold tracks lagging indicators downstream of the causes for those indicators, I think it rarely makes sense to buy gold if you have a deeper, more targeted insight. In the 1970-2020 backtest, commodities have an inflation beta of 4 vs gold’s 2, which is matched with far less volatility by TIPS. Oil futures from 1983-2020 have an inflation beta of 7.9 vs gold’s 1.9 for 1975-2020.

What it takes for gold to really move, why I remain tepidly bullish, and how I’m positioning

Gold’s indifference may be attributable to the fact that it is fundamentally a mimetic asset. Without cashflow, there is no immediate framework for ascribing valuations (explaining gold’s short and long term divergences from it’s fundamentals), and no market based corrective mechanism (if cashflows are undervalued, dividends and buybacks create buying pressure that reduces valuation divergences relative to other assets). Gold is worth only what another buyer will pay for it, and is reliant on the mimetic desire of future speculators.

Mimetic assets are perpetually in competition for a limited pool of animal spirits and greater fools, and gold has simply been outcompeted by bitcoin and ponzi tech the last decade. For gold to move, a paradigm shift has to occur for a bubble to begin.

While I caveat that it’s impossible to identify the exact timing and nature of such a paradigm shift, gold’s macro drivers (debt, money supply, geopolitics, etc.) are all moving in the right direction. There are signs that gold is being relegitimized (see below) and net positioning in gold is very low relative to risk-on (general equities) and risk-off (bonds) assets, many of which face structural headwinds (withdrawal of liquidity, inflation). A small reallocation could greatly impact the gold price.

However, it’s unlikely I will ever make an allocation to either physical silver or gold, as I believe there are assets with more predictable and powerful catalysts. I will only consider silver equities, as I believe PMs are purely bubble assets and silver is a thinner market with a better supply picture and a stronger cult backing it. I do hold a small position in Kuya silver and Discovery silver due to idiosyncratic factors, and I will consider adding to them on a 20% dip (they are cheap, but not as cheap as some other things I am looking at). A brief list of silver’s bull factors (with caveats):

Silver is still down ~2/3 from its peak in 1980 (But that was also a speculative bubble - most dotcom stocks never recovered. And much, such as supply demand dynamics, can change in the interim)

Average primary silver miner grades have essentially fallen in half over the past 20 years, and prices are now nonsensically below all-in sustaining mining costs (Again, silver does face the same stock to flow and investment vs physical demand issue mentioned above, albeit to a smaller extent. Industry AISCs are also not easy to estimate. This needs to be verified)

Solar and green transition is going to greatly increase silver demand (I agree on this one, but I suspect the ESG transition will be slower than many think)

COMEX and LBMA silver inventory has collapsed this year (Ok, but people have been calling for this forever. When does it matter?)

Positioning by speculators is max bearish (Again, something that has happened several times before with false starts. We are also heading into tight liquidity conditions)

Final thoughts

It's been frustrating investing in the space, and no one can tell if the pain will be over soon. The narratives for gold are grandiose, but things could take a lot longer (reshoring could be far off, inflation could taper off and USD reserve status will not go away immediately, for e.g.) and be a lot more uncertain (geopolitics is unpredictable). I think the probabilities for a singularity event (e.g. pervasion of stagflation in popular consciousness) for gold is rising, but I would still suggest only a moderate allocation to it, as a long dated call option on macro tail risks.

To any investors in the space, I would suggest that gold bull markets are particularly volatile and difficult, or nearly impossible to time. If you want to buy gold, keep your eyes for incredible buying moments, be patient and don’t lose your sleep over the day to day. And buy silver for more torque.

Some useful links

There has been work on timing the gold market using the business cycle (although it remains if the same timing mechanism produces superior and more predictable returns in a different asset class) and trend following (which is consistent with the view of gold as a mimetic asset).

This provides a useful overview on the metals equities that offer more leverage to the theme.

Great summary. Posted it on Reddit.

https://www.reddit.com/r/Wallstreetsilver/comments/yq0fv9/waiting_for_goldot_a_great_unbiased_synopsis_of/