Disclosure: I am a generalist, recently graduated retail investor who seriously entered markets in 2021. ALL of my research is borrowed from others (see references), I claim no credit for it, and merely intend to consolidate it for others to learn more about a sector.

Contents (Part 2):

How I see the sector and equities performing in the future

Idea 1: Glass House

Idea 2: Marimed

Idea 3: Verano

Broader risks

Closing thoughts

References

How I see the sector and equities performing in the future

While Cannabis equities could go down further, valuations are cheap, and due to the inefficiency in the market, stock picking can be rewarding. I’ll go through some high level catalysts/factors for outperformance in the future, before discussing specific equities in the next section.

Earnings will continue to grow

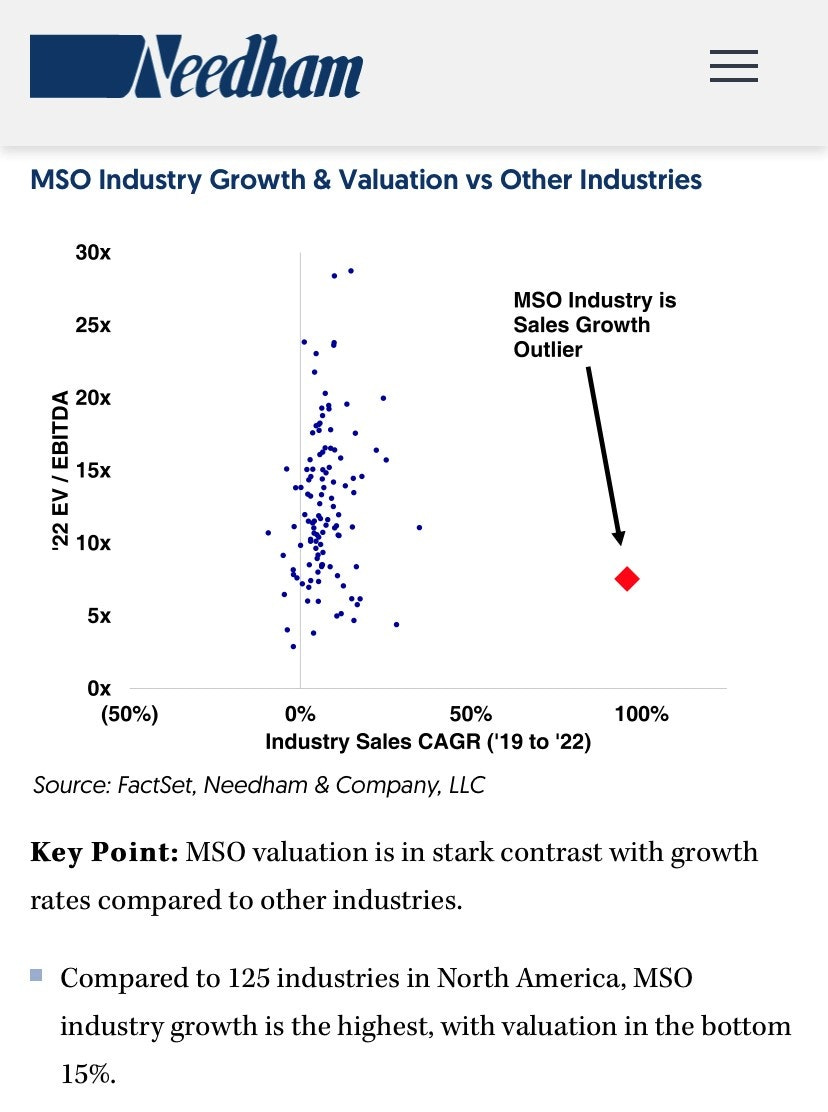

As discussed in Part 1, overall demand for Cannabis is increasing, and the legal market is cannibalising the illicit market. Even at extreme discounts to recent growth rates (Fig 13), legal Cannabis will likely grow at least 20% (discount from 40% estimate by Merida Capital in 2020 - discounting is valid because MSOs can create inorganic growth through acquisitions).

Hence, even if multiples stay constant, earnings growth should drive returns over time.

Multiples will rerate as institutions and adjacent industries enter the space

Institutions and other companies are already waiting to enter the space, and when they do, multiples will rerate higher. BlackRock president Rob Kapito said: “We will be investing [in cannabis] but because of issues with states and the U.S. federal government, some of our custodians will not clear cannabis stocks and we will have to wait until that happens.” Coca-Cola, British Tobacco, AB-Inbev, Nestle are all exploring the space.

How much higher can multiples rerate? Note that there are no restrictions on owning Canadian Cannabis companies, and Vanguard, Blackrock, TIAA-CREF, State Street and others already own Canadian Cannabis majors. In 2020, with lower growth and profitability, they traded at ~3x higher Price/Sales. British Tobacco paid ~9x sales in 2020 for 20% stake in Canadian Cannabis firm Organigram, when it was still loss making.

The entry of institutional and corporate investors will likely only come with federal legalisation.

Federal legalisation is an upside risk and is a when, not if

I don’t think anyone can predict the exact path and timeline of federal legalisation, but the equities are priced as if it will take a long time, whilst political tailwinds continue to grow.

As mentioned in Part 1, there is already bipartisan voter support for legalisation. Politicians on both sides have positioned accordingly. In 2018, Mitch McConnell pushed to legalise Hemp. South Carolina representative Nancy Mace is introducing the State Reform Act which will remove Cannabis as Schedule 1, and has obtained support from her Republican colleagues. Republicans like Senator Steve Daines have flipped. Even Alabama is legalising medical use. And democrats have always been vocal about legalisation, with Biden promising descheduling and decriminalisation. There is also support from neutral parties like Janet Yellen.

With bipartisan support, why has federal reform stalled? The primary reason has been gridlock. SAFE Banking was the primary federal reform bill in discussion the past few years. It would make it illegal to penalise banks from working with Cannabis companies, opening them to banking service and institutional investment. It passed the House 6 times, with 321 to 101 votes in Apr 2021. However, it was shot down by democrat Chuck Schumer, who pushed a more aggressive reform bill. It was speculated this was done to satisfy progressives who criticised SAFE as too conservative when Schumer was running against progressives for re-election.

I am not an expert on US politics, and I think most “expert” forecasts are poor. What I will say is that equities are overly pessimistic on the chance for reform. Both democrats and republicans want some kind of reform, the debate is on what exactly. Pressure is mounting: Ed Perlmutter threatened to derail the defence bill in response to SAFE being left out. Post re-election, Schumer no longer has to worry about pleasing progressives. New bills like the State Reform Act offer different paths to legislation. So the truth is, reform could take anytime from 5 months to 5 years, but it will likely happen at some point, and I don’t want to miss the rerate.

How much reratng? Bright Green (BGXX) was the first US Cannabis company to IPO on NASDAQ in May 2022 after receiving special federal clearance. It jumped briefly to a valuation of 8B. For perspective, that made it the most valuable US Cannabis company while being pre-revenue, vs peers with strong balance sheets and positive free cash flows. I can’t predict exactly how much, but it will be significant.

Rerates have happened without legalisation

Market mood is like a pendulum. Looking at the chart of US Cannabis companies, they have traded at much higher levels without legalisation before.

Delayed legalisation is not a bad thing

There are huge companies in Alcohol, Tobacco, and Consumer goods industries that are looking for growth. Had they not been deterred by federal regulations, they would likely have dominated the space early on due to superior expertise and resources. Instead, Cannabis companies have had years to build expertise and infrastructure from seed to sale. The runway for growth is still long. Federal illegality will allow them to take more market share and build stronger moats. Legalisation delays benefit the best US Cannabis companies, justifying higher valuations when legalisation eventually comes.

Idea 1: Glass House (OTCMKTS: GLASF)

*Note that my three long ideas were inspired by Aaron Edelheit. I supplemented his research with my own

Glass House is a Californian cultivator, with a small retail presence. It is operating a 500,000 sq ft greenhouse in Santa Babara. It just acquired the second largest greenhouse in America, and the largest one approved for Cannabis, with 5.5m sq ft. I’m bullish on it because they are able to produce high quality flower at the largest scale and lowest cost in the country, and the Californian market can absorb their produce. Interstate commerce is probably far away, but if allowed, Glass House will be a top supplier for the US market. Their cultivation expertise, scale, and retail integration also makes them excellent partners in developing Cannabis branded products. Overall, Glass House is positioned to generate massive cash floats and build moats across the supply chain.

We’ll go through the key bull points:

Glass House can grow Cannabis at a scale, quality and cost that none can match

How do Glass House’s costs compare? Cannabis is a difficult plant to grow. Outdoor Cannabis is cheap but poor quality. Indoor Cannabis is high quality but extremely expensive. Greenhouse Cannabis is a middle ground, but climate dependent. Glass House’s greenhouse is in Ventura, CA, with one of the best weathers for agriculture. It’s greenhouse is state of the art and was optimised for the highly competitive tomato market, and is now being adapted for Cannabis. Even before acquiring this greenhouse, Glass House cultivation costs were ~$180 per lb (Fig 14 left hand side), which they aim to bring down to $100 per lb (Fig 14 right hand side) at the new greenhouse. For a small Californian farmer, the costs are ~$350 per lb, and the lbs could be lower quality as they are mostly outdoor vs greenhouse. Cultivation costs are even higher outside California. In Colorado, a mature Cannabis market, cultivation costs average $800-$1000 per lb including taxes (small farmer in California is $500 per lb including taxes). The average MSO cultivates for $700 per lb.

Besides the massive cost advantage, Glass House will have a quality advantage as well. Even before operations at the new greenhouse, Glass House moved up to #1 flower brand in California as of July 2021. And Californian Cannabis is among the best in nation. Illicit dispensaries in other states are full of Californian products, and California exported 12.7M lbs of Cannabis in 2019 (total 2019 US production was 30M lbs).

Glass House will also have tremendous scale. Assuming current Glass House yields and with the new greenhouse, they have a total capacity of 1.7M lbs per year, almost 6% of 2019 total US production.

This is unlikely to be competed away, either in state or out of state. There aren’t that many greenhouses of this size (it’s the second largest in the US), and it’s practically impossible to build new greenhouses or get them approved in California, much less for Cannabis. And California’s weather cannot be replicated.

Enough demand to absorb all the Cannabis Glass House wants to sell

California is the largest Cannabis market, almost as large as the next 3 combined. Market size was estimated to be 4.8M lbs in 2019, with 1.3M lbs sourced in state legally, 3.3M lbs sourced in state illegally, and the rest imported. In 2019, there were less than 700 dispensaries (critical for access to legal market), but now there are 1024 (46% increase). Sales grew from 2.8B in 2019 to 5.2B in 2021 (~86% increase). Assuming conservatively lbs sold increased 35%, current annual lbs would be 1.75M lbs. While the greenhouse at total capacity would be almost the entire current legal market, the greenhouse will take years to bring online. Phase 1, which is planned to be completed by 2023, will triple capacity to 270,000 lbs, and is only ~15% of this 2021 figure. By 2025-2030, the Californian market would have grown, and if some restrictions on interstate commerce are lifted, Glass House could sell to the broader US market (California exported 12.7M lbs of illicit product in 2019).

Furthermore, Glass House’s license moat, incredible costs and high quality means that they will likely take a much larger market share in California. It is not uncommon in agriculture for cost advantaged producers to take significant double digit percentages of regional markets.

There are also tailwinds for growth in California’s legal market.

Legal demand has been artificially suppressed due to state restrictions on retail licenses, which are fast liberalising. 57% of Californian cities and counties do not allow any Cannabis businesses. California had 830 licensed dispensaries in Jan 2022, the same as Colorado, with a population of 40M (vs 7M). Without access, per capita Cannabis spending in California is less than half of Colorado (Fig 15). However, the rate of issuance has been increasing due to political pressure. There were 35, 60 and 30 licenses issued in California in Q2, Q3 and Q4 2021 respectively. But from Jan to Jun 2022, 15 cities have repealed bans and 194 licenses have been issued. Many of these stores are in areas with no other dispensaries (meaning disproportionately large sales) and will open in Q3 2022. Glass House has 6 dispensaries of their own, which they plan to grow to 10 in 2022, which is key as they sell 15x of their own product in their own store than other stores.

Legal demand has also been suppressed by the cultivation tax on legal Cannabis, which makes it uncompetitive with illegal Cannabis, but taxes are likely to be eased going forward. California Cannabis is taxed 4 ways: a $160 per lb cultivation tax, which is compounded by a 15% state excise tax, 8-10% local tax and a sales tax. This does not include things like license fees. Legal Cannabis can be twice as expensive as illegal. But the pressure to remove the tax and watch out for small farmers is mounting: Governor Newsom included a removal of cultivation tax in his budget proposal. ***Note on July 2 2022: Effective immediately, Governor Newsom removes Cannabis cultivation tax and will not raise excise tax for at least 3 years and shifts it from the distribution to retail level. This will make the legal market far more competitive with the illegal market.

Increasing crackdowns on illicit dispensaries have also redirected more demand to legal businesses.

Overall, California is a large market with significant runway for growth, that can absorb all of Glass House’s product for many years.

Supply situation is improving in California

In 2021, due to massive overproduction, the Californian market collapsed. Prices fell from ~$1200 per lb to ~$400 per lb. Farmers are having produce returned as distributors cannot sell it. This is below the average small farmer’s cost of $500 per lb. The pain extends to large firms, with firms like Harborside reporting a -30% gross margin (Glass House also suffered, with margins falling to 14%).

Suppliers are cutting back. The founder of Curaleaf hears that “50% of farms are not being leased this year”. Cresco wrote down its California assets by >$250M and is scaling back Californian wholesale operations. The Parent Company wrote down >$500M of assets. Curaleaf has divested it’s Californian cultivation operations. Glass House was buying equipment from cultivators at 50 cents on the dollar.

California is also looking to phase out its provisional license (72% of legal market), by 2022, meaning entrants will have to apply for an annual license (which could months to years) or purchase incumbents to enter. This should restrict the supply side further.

Also, the worst glut was in the outdoor market, which is a different tier from the greenhouse market (with much higher barriers to entry) that Glass House solely operates in. There is new cultivation capacity coming online in 2022, but almost exclusively in the outdoor market.

Having survived an extinction event in Californian Cannabis that is leading to supply cutbacks, Glass House is likely to benefit from a more balanced market going forward.

Strategic position for brand development

Cannabis will evolve beyond just the flower itself, and Glass House is well positioned to develop Cannabis brands. Their scale, quality and retail presence allows them to bring products from experimentation to production. The company has been developing and testing products based on feedback from their stores (e.g. sleep and pain tinctures), and has collaborations to create new products (slide 20-23). In the future, they would make ideal partners/acquirees for large firms like AB-Inbev that are trying to break into Cannabis.

Skilled and aligned management

Co-founder and president Graham Farrar was a successful 3 time entrepreneur before Glass House. Co-founder and CEO Kyle Kazan is a PE manager who has started 23 funds with combined AUM of 2.75B. They started Glass House in 2016 and have scaled production and closed an acquisition of a killer asset.

Share structure and compensation means management is aligned. When they were acquired by SPAC Mercer Brands, the management team and founding investors rolled all ownership into equity. Graham and Kyle own 11,981,559 out of 61,955,414 shares (19.3%) of the company, and each has individually 800,000 unvested shares and 200,000 in options. Salary is ~350,000 for both, meaning compensation is mostly stock based. If company EBITDA exceeds 55M for any 3 month period, all executives will have 25% equity incentives Company accelerated.

ESG

Glass House has high ESG ratings, which is important for institutional participation.

Valuation analysis

***Note on July 2 2022, cultivation tax has been removed in California, adjust below figures accordingly.

Glass House (OTCMKTS: GLASF) trades at a $2.6 as of June 27 2022, with ~62M shares issued and outstanding as of Q1 2022, for a market cap of ~161M. Fully diluted share count is ~107M including exercise of ~33M warrants at $10-$11.50, which would bring in 300M in capital.

As of Q1 2022, it has ~21M in cash, ~206M in property/plant/equipment value, ~45M in long term debt, with Asset-Liabilities of ~163M, which is equal to current market cap.

Glass House is currently producing 90,000 lbs of Cannabis, and is targeting a Phase 1 expansion which will add 180,000 lbs of capacity. What would gross profits look like then? Assume: 1) cultivation tax stays the same (pro forma $98 in Fig 14), 2) Cannabis prices are at ~$500 per lb (lower than average price of $591 during 2021 glut) and 3) cultivation costs are per Fig 14 (2 different figures for 2 different greenhouses). Gross profit would be (500-179-98) x 90000 + (500-128-98) x 180000 = ~ 69.4M.

That said, operating expenses for the company are significant. It was 51M for 2021 (Fig 16). General and Administrative costs accounted for 33M, increasing 81% YOY due to expansion costs, such as 8.3M going to compensation and IT consulting fees. Professional fees accounted for 9.4M, increasing 345% YOY due to one off needs like applying to licenses, SPAC merger and greenhouse acquisition. Depreciation and Amortisation accounted for 4.7M, due to increased asset value.

Latest operating expenses are 15.5M for Q1 2022 (Fig 17). To lower bound actual running costs, let’s say 4M of 9.4M General and Administrative (most labour costs should already be in cultivation costs) and all of Sales and Marketing are recurring and scale linearly (no economies) with capacity. Assume Professional fees are one off and fall to 2M (2020 annual figure). Depreciation and Amortisation is annualised. Operating expense would be (4+0.86) x 3 x 4 + 2 + 2.6 x 4 = ~70.7M. Operating income would be ~0.

Hence, at current stock price, and with conservative assumptions, the company is trading at net asset value (primarily in property value), but not making money.

In a more realistic scenario, let’s say: 1) tax stays the same, 2) price rises to $700 per lb (below $1250 per lb high in Aug 2020, and the price for top quality greenhouse flower in Feb 2022), 3) cultivation costs stay the same, and 4) new greenhouse produces 300,000 lbs per annum. Gross profit would be (700-179-98) x 90000 + (700-128-98) x 300000 = ~ 180M. Increasing G&A and S&M costs proportionately (39/27), while holding Professional fees and D&A constant, operating expenses would be ~96.6M. The company would have an operating income of ~83.4M a year, 52% of current market cap. This scenario assumes no political change, pricing at long term average, and market share at ~20% of 2021 figure. The company is still ~2x operating income (let’s say 2.3x with dilution) and cheap.

One can play with the numbers, but it’s clear that if cultivation tax falls, volume increases or prices rise, the cash flows increase dramatically. And note that Glass House is a call option on interstate commerce: being able to produce 1.7M lbs per year at the lowest cost and highest quality in country will lead to cash flows that would justify a multi billion valuation. Note also none of this includes the upside from venturing into brands and retail, or the full margin capture from Glass House owning their own dispensaries.

Concerns:

Operating expenses

This is my biggest concern, especially since there is little transparency over operating expenditure numbers. Is management prioritising growth over frugality? Is it one off? I would like more visibility into this in future conference calls and will write about it again.

Competition from the Illicit market

***Note on July 2 2022, cultivation tax is removed, bringing legal producers $150 closer in cost to illegal producers.

California exported 12.7M lbs of illicit product in 2019. How can Glass House compete against that? Firstly, it does not have to, as it can out-compete the legal market. Secondly, it can, due to its cost and quality. Note that the illicit market is cheaper only because it evades all taxes. Their main objective is not getting caught, not cost, and being illegal, they have natural limits to scale. But admittedly in the medium term, California being the heart of illicit market supply does present greater headwinds. That said, we have seen the California market grow greatly despite that, and there is still a lot more retail penetration to come.

Volumes and inventory levels will be key to watch to see if Glass House can sell all its product.

California slowdown

Glass House can earn market share in state. And with low dispensary penetration, high taxes and an enormous illicit market, the long term runway is still great. Politicians are also incentivized to phase our the illicit market as they dodge taxes.

Expansion delays

Operational challenges could slow down Glass House. Whole host of problems could occur, such as lack of talent. Glass House’s COO just left (Cannabis industry has high turnover). That said, the team has had experience running greenhouses at scale with low cost, and the most difficult challenges like licensing are solved. It’s a matter of time. The challenges facing Glass House would also face most Californian cultivators.

Cost inflation

This will hit all producers, including illicit ones, raising prices. Also, Glass House’s cost advantages would be even more important.

Dilution risks

With significant costs from expansion (as seen in the operating expenditure), dilution could be significant. However, the price is still be attractive as per calculations above that assume some level of dilution.

Oversupplied market

Could the California market crash again? The winding down of operations by large operators and small farmers, and the barriers to entry for greenhouse cultivation, mean the market should re-balance. And overall, agriculture is cyclical, but Glass House is cheap assuming long term average pricing. That long term average pricing may come down over time, but it would likely be due to highest cost producers being forced out, lowering the market clearing price, which should also mean higher volumes for Glass House.

Margin compression

In commodity businesses, margins tend to compress over time as new players enter and the product is not differentiated as it is a commodity. For Glass House, in the short term, there are no equivalent greenhouses (which produce higher quality flower than outdoor), and Glass House is building brands at both the flower (Already #1 flower brand) and product level, which will provide differentiation in the future. In an interstate situation, Californian growers will dominate the industry due to weather and soil that cannot be replicated.

Political risks

There’s always a chance California becomes even more unfriendly to Cannabis. However, the extinction event in California in 2021 has pressured politicians and it seems like the tailwinds are for less, not more onerous legalisation. Valuations are still cheap without assuming a removal of cultivation tax.

Summary:

Glass House has an unparalleled asset that could produce enormous cash flows at modest prices and without state help. It is one of the few survivors in an extinction event, meaning it will enjoy a more balanced market in the future. It has huge runway to grow, being in the largest Cannabis market in the world. It’s main risks are operational roadblocks and cost control during expansion.

Idea 2: Marimed (OTCQX: MRMD)

Marimed is a MSO with footprints in 6 states. The bull case for Marimed is that it is the cheapest MSO, due to structural reasons barring investor ownership, and is going to grow significantly in the states it operates in.

We’ll go through the key bull points:

Marimed has uniquely bad capital market access

We spoke about the issues US Cannabis companies face in capital markets. Marimed faces this to a greater degree, because it cannot even be owned by $MSOS. $MSOS can only own US Cannabis companies which have a Canadian listing, which Marimed does not. MariMed has filed for a Canadian listing, and if that succeeds, it should lead to buying pressure from $MSOS.

Furthermore, the company only started significant efforts to court investors in Oct 2021, causing them to be widely unknown.

This explains why valuations are so cheap, and could rerate upwards in the future.

It’s cheap

As of Mar 2022, it 335.6M shares outstanding, 437.8M fully diluted. As of Jun 28 2022, it trades at $0.47, for a market cap of 157.7M.

As of Q1 2022, Marimed has ~33.5M cash, ~65.5M Plant, Property and Equipment, and Asset-Liabilities of ~81.3M. From 2020 to 2021, Cash and cash equivalents grew by 10x from 3M to 29.7M, and total assets grew by 60% from 76.4M to 123.2M.

For 2021, revenue was ~121.5M, adjusted EBITDA was ~$43.1M. The growth in revenue and EBITDA from from 2020 was 139% and 144% respectively.

At 1.3x trailing sales, 3.7x trailing EBITDA, with a net cash and net asset position, and with a high growth rate in a growing industry, Marimed trades like a dying company.

Even if we adjust EBITDA by adding back depreciation and amortisation, interest and taxes, but holding other adjustments (almost exclusively amortisation of options) constant, we would have 21.7M, so ~7.6x trailing earnings. Fully diluted (over adjustment for amortised options), it would be ~10x. For a high growth company (and all growth thus far was unlevered), that is not unreasonable.

Meanwhile, Marimed is expanding its footprint across multiple states, which mean revenue and earnings should continue to grow in the future.

Expansion in Illinois

As per Dec 2021 estimates, Illinois and Massachusetts accounts for 83% of Marimed’s revenues.

Marimed currently operates 4 dispensaries in Illinois.

They have acquired a license for cultivation and are currently constructing a growing/production facility which is expected to be completed in 2023. They plan to distribute product through their own dispensaries, which would increase revenue and margins.

They also plan to open 6 more dispensaries (up to the state dictated maximum of 10 for any entity), although the timing is not announced. These dispensaries would likely be very profitable as Illinois is severely underserved. Illinois’s per capita spend on Cannabis is as low as California (Fig 15), since it has only 110 dispensaries for 13m people (a 1/3 of California’s ratio). Even after lifting a stay on licenses, allowing 185 more dispensaries to open, the per capita dispensary count would still just be on par with California.

Marimed also owns Bettie’s Eddies, the #1 edible brand in Massachusetts and #1 in Illinois until 2019 when it lost it’s state distributor, and plans to reintroduce it to the state.

Expansion in Massachusetts

Marimed currently operates 1 dispensary and 1 cultivation and processing facility in in Massachusetts.

They are planning to open 2 more dispensaries (up to maximum of 3 per entity in Massachusetts) by late 2022, which would likely be profitable as Massachusetts is also underserved with 165 dispensaries for 6.8M people.

They also plan to expand their cultivation facility by late 2023, which would increase revenue and margins.

Expansion in Maryland

Marimed has 1 cultivation/processing facility in Maryland.

They have fully acquired the cultivation/processing facility and plan to use it to full capacity. The facility was under a managed services contract with KIND, where only 100,000 out of 180,000 sq ft was used. After a long dispute, they have finally managed to acquire KIND. They will now benefit from better economics by fully using the facility, and almost double cultivation capacity.

They also have 1 dispensary in Maryland that will come online in 2022. Maryland is underserved, with 102 dispensaries for 6M people.

Maryland also has further regulatory upside. Maryland currently only legalises medical use. Maryland state legislators have approved a ballot initiative for adult use for the November election. The governor has stated he will not block legalisation. Adult use could come to Maryland in 2023 or 2024. And adult use usually doubles or triples the market size. With one of the largest cultivation facilities in state, Marimed will benefit.

High value brands

Marimed owns several top brands, such as: 1) Nature’s Heritage, the #1 flower brand in Massachusetts, 2) Betty’s Eddies, the #1 edible in Massachusetts, #1 edible brand in Illinois until 2019 when distribution stopped, and awarded “Leaflink’s best medical product in 2021”. Betty’s Eddies has sold 1.8M chews by Q3 2021, and has received acquisition offers.

It’s Illinois dispensary was also awarded “Leaflink’s top dispensary for 2021”.

Additionally, Marimed is developing new products, such as THC drinks.

This portfolio increases volume and pricing power, and has acquisition value.

Valuation revisited

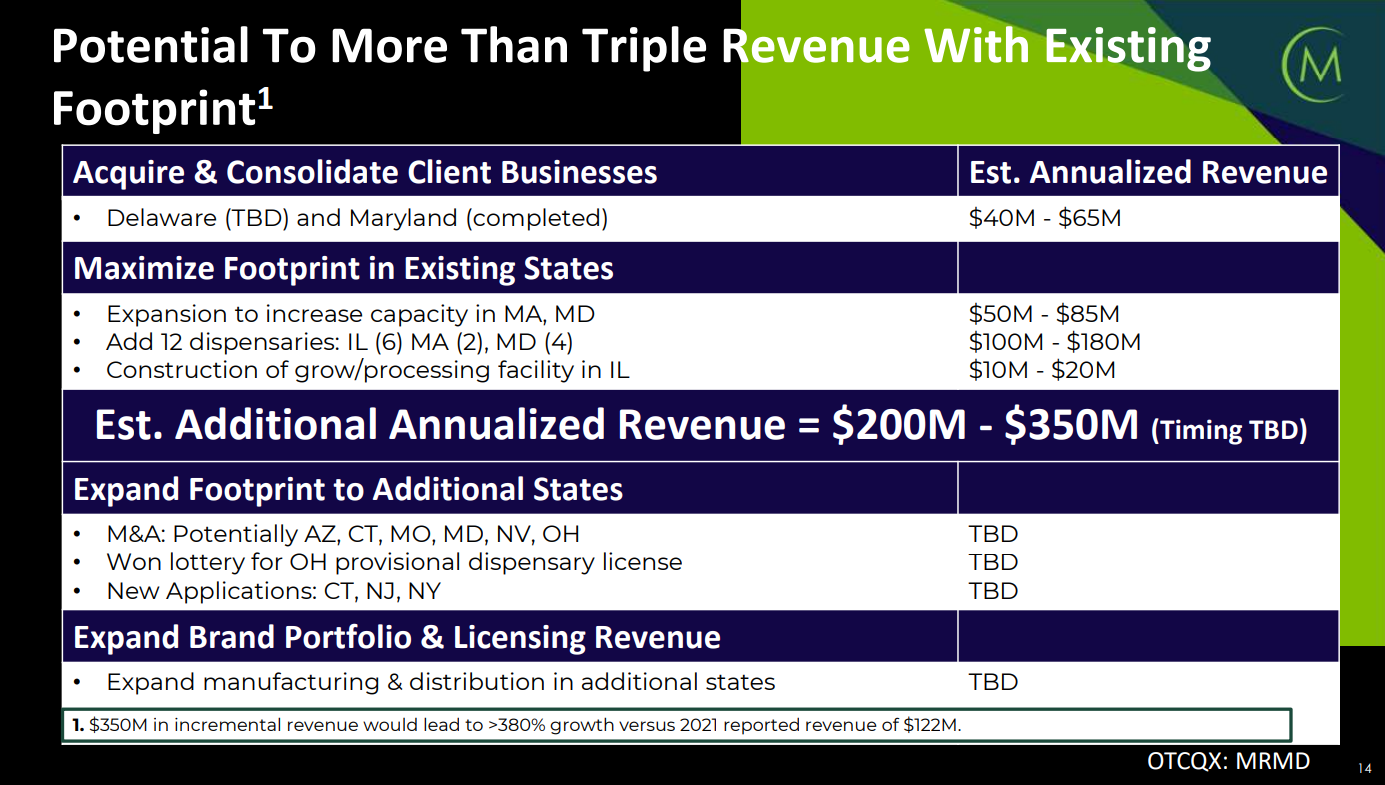

Even without any growth, Marimed’s valuation of 3.7x Price/EBITDA is cheap. But it’s main states Illinois, Massachusetts and Maryland are expanding. It has won a dispensary license in Ohio. In Delaware, they are expanding cultivation by 40,000 sq ft. It is in multiple M&A discussions for growth. The company sees a clear path to triple revenue over the next years (Fig 21). And they have lived up to their promises before: in 2021, it was the only MSO that raised and beat it’s raised guidance.

I believe the general direction for earnings and revenue is up, and some of those catalysts will occur in 2022 (e.g. first dispensary in Maryland).

Risks

Operational risks

Operational risks can derail Marimed’s plans. However, the state’s main expansions are in states they are familiar with. It may slow things down, but it is very likely Marimed will eventually hit their expansion targets, especially since litigation and licensing issues are mostly out of the way.

Cyclicality and margins

Could a California style supply glut hit Marimed? With all MSOs increasing cultivation in Massachusetts, prices have started to come down in latest earnings reports. But the impact is likely more muted for Marimed. With vertical integration, strong brands and because they are opening dispensaries in underserved states, Marimed’s cost structure, pricing power and less competition will help them survive. It is also important to note that the size of the illicit market is much smaller on the East coast, and licensing for both retailing and cultivation is a lot more limited (California is unlimited license for cultivation and has a huge illicit market), which means supply is unlikely to increase to the same extent. As long as these factors don’t change, East coast operators like Marimed will likely still be profitable (some long term compression is to be expected).

Furthermore, brands will be important in creating pricing power in the future. Marimed, as owner of top brands, has shown an ability to develop and monetize branding, which is key to moving out of the commodity flower business.

Interstate commerce

In an interstate commerce scenario, a smaller MSO like Marimed may struggle to compete with larger or specialist firms. However, interstate is likely far off, and in the meantime Marimed is expanding in scale.

Idea 3: Verano (OTCMKTS: VRNOF, CNSX: VRNO)

The summary on Verano is that it is profitable, with industry leading margins, strong growth, and yet the stock trades at a discount to it’s less well run peers. It’s undervaluation is probably a combination of management under-promotion, under-investment by $MSOS, and because shares locked up post IPO were allowed to trade. For more information, refer to Todd Harrison or Aaron Edelheit’s posts on Verano, or just search the company in Seeking Alpha.

Broader risks

We went over specific companies above, but I will talk more briefly about risk across US Cannabis equities right now.

Business fundamentals are to be assessed at the state and firm level, not industry level

More of a pointer than a risk, but note that there is no United States of Cannabis. Each state is it’s own island, and while interstate commerce ban may be unconstitutional, the ban will probably take a long time to lift as Cannabis companies pay so much tax that most states (and their politicians) will be protectionist.

Hence, beyond federal reforms with universal business implications like SAFE, there is no “industry level analysis” of Cannabis to speak of. All risks must be assessed at the level of the firm and the states it operates in.

Federal reform risk

That said, federal reforms such as SAFE are meaningful to the investor. Hope of Biden reform was one of the reasons why $MSOS rose till its peak in Feb 2021. Institutions allowed to invest will rerate equities higher. What if reforms don’t occur?

But to me, at these valuations, and considering the repeated failures of SAFE (6 times it passed the House, 6 times it failed), it looks like the market has priced in a very low probability of near term reform. The risk is now to the upside.

Broader market risk

Markets are in deep fear right now. All equities are selling off. This includes US Cannabis companies. And I think there could further declines. But I think it’s hard to time the bottom, especially in a sector where valuations are already so low. I think at the very least, it’s a sector worth watching, and if a deeper selloff comes, it may be an excellent chance to accumulate. And in the recovery, it will be profitable, growing companies that will rally the most.

Canadian Horror Story

Canadian cultivators expanded ferociously in 2016 and 2017, collapsing prices and leading equities in a 92% decline. Admittedly, every single US Cannabis company is expanding. Will we have an American Horror Story as well?

I think this is a valid concern, but I think the US market is different because the regulations make it so difficult to start a company, and there are often artificial restrictions on supply. This analysis has to be brought to the state level. And the right companies will do much better under adverse conditions. For example, Glass House is expanding with positive gross profit in the worst Californian supply glut, while large competitors like Cresco, Curaleaf and The Parent Company are withdrawing. Picking the right state and the right stock is key.

Consumer discretionary vs staple

There are fears of an extended recession. Some consider Cannabis a consumer discretionary which will be disproportionately hit, and consumers tend to switch to cheaper illicit product when they feel poorer.

No doubt, a recession would reduce earnings, especially for high end, expensive flower. However, I think the runway for growth is so large that the industry likely maintains its trajectory through a recession. Besides, companies are so cheap now that they don’t need massive growth to justify valuations.

Compressing margins, slowing growth

There are always reports that the Cannabis market is slowing down or will grow slowly.

That day will come, but we are not close. Consider Colorado, the first state to legalise adult use (2012). Sales had reached 1.5B in 2018, 6 years after adult use, and yet it kept growing to 2.1B in 2021, with projected 2.2B in 2022. Consider that 1) the illicit market is still 3-4x the size of the legal market, 2) there are still states moving towards medical use, 3) many states have 5-10x less dispensary counts per capita than Colorado, and 4) Cannabis is seeing growth in multiple uses, and it’s clear that this is still a largely nascent industry (even more so in some states).

Margins will come down over time, but the best companies will remain highly profitable. Todd Harrison has an excellent piece discussing margins over time and the profile of companies (that look a lot like Glass House) that will succeed. There is huge disparity in company quality in this sector, and stock picking is key.

Closing thoughts

It’s been a long post, so I’ll make this short. After a 16 month bear market, stocks are very cheap, and sentiment looks like despair (just search “$MSOS” on Twitter). With expectations so low (could go lower), surprises start to skew to the upside. And US Cannabis is structurally underowned, meaning 1) a highly inefficient market and 2) there are more buyers on the sidelines than sellers. Stock picking is key, and I believe Glass House, Marimed and Verano are cheap in a cheap sector, and can justify their valuations under modest conditions.

Of course, more bad things can happen in Cannabis, and some are likening this equity selloff to the great depression, but if not averaging in now, I believe this sector is at least one to watch.

Disclosure:

I am personally long 38.5K $MRMD @ cost basis 0.6, 2.25K $GLASF @ cost basis 2.04, 700 $VRNO @ cost basis CAD 9.76

References

Todd Harrison, a seasoned hedge fund manager that runs Cannabis fund CB1 Capital, and has explored the space for more than a decade. Has a fund blog, a substack and a twitter. Might be a bit too bullish, but extremely knowledgeable. Might be the most knowledgeable on medical Cannabis.

Aaron Edelheit, a seasoned hedge fund manager that has launched the Mindset Value Cannabis Fund. Has a substack and a twitter. I copied his work the most. Follow him if you want to follow the three ideas above.

Hirsch Jain, founder of Ananda Strategy, a Cannabis consultancy. Very well versed in the space, especially California. Has a twitter, and has many interviews on Youtube and Seeking Alpha.

Emily Paxhia, who runs Cannabis fund Poseidon Asset Management and has invested in the space since 2014. Very well versed in the space. Has a twitter, and has many interviews on Youtube and Seeking Alpha.

Mitch Baruchowitz, who runs Cannabis fund Merida Capital. Very well versed in the space. Has interviews on Aaron Edelheit’s substack and on Youtube

Seeking Alpha is a good resource, for both bull and bear sides of Cannabis. Search “Cannabis” or the ticker you wish to investigate.

Graham Farrar, co-founder of Glass House. Gives a founder and operator’s perspective. Has a twitter, and interviews on Aaron Edelheit’s substack.

Conference calls of companies in the space are excellent to understand the states they operate in.

Great write up